Before doing the calculations of the income tax in India, the very first and most important point is to know what is to be considered as the “salary”. Section17 of the Income Tax Act, 1961 itself carries a specific and comprehensive definition of the terms salary, perquisite, and profits in lieu of salary. Of these, salary as per section 17(1) is the very base on which all salary-related tax calculations are constructed.

Understanding salary as per section 17(1) of income tax act is non-negotiable if you are a salaried employee trying to decode your Form 16, a CA student preparing for exams or an HR professional calculating TDS u/s 192. This guide will teach you everything from what it is and what it comprises of, to practical examples, comparison tables, and frequently asked question answers.

What is Salary as per Section 17(1)?

Salary as per section 17(1) means a specific kind ofsect with receipts obtained by an employee from an employer and its connected items in relation to the business carried on by that employer. It does not just cover the basic monthly salary – it extends to all payments such as wages, annuities, pension, gratuity, fee, commission, allowance and other forms of payment.

The section 17 is bifurcated into three categories under the Income Tax Act.

- Section 17(1) – Defines “Salary”

- Section 17(2) – Defines “Perquisites”

- Clause (3) of Section 17– Profits in lieu of Salary

The problem is that salary as per section 17(1) also covers employees that are not in the private sector. It is equally applicable to government employees, pensioners, contractual workers getting regular remuneration and even an office-holder of profit under the Constitution.

Read Also:- Pilot Salary in India | Air Hostess Salary in India | CA Salary in India

Salary as per Section 17(1) – Complete List of Inclusions

salary as per section 17(1) under the IT Act shall be defined as follows:

1. Wages

Any consideration received for the performance of services, including cash, fees, or minimum pay, skall considerede. This is the most default source of income for salary workers.

2. Any Annuity or Pension

According to Salary as per section 17(1) includes pension, drawn from an earlier employer. This is a vital point pension is specifically mentioned in the definition. As a result, pensioners are taxed under the head “Salaries” and not “Other Sources,” unless the pension is received from a non-employer (i.e., NPS from government).

3. Any Gratuity

Gratuity receiving while in employment (i.e., not on retirement) is covered in the definition of salary under section 17(1). Although they may be exempt under Section 10(10) for gratuity received at retirement,

4. Any Fees, Commissions, Perquisites, or Profits in Lieu of Salary

- Fees: Extra payments for particular services.

- Commission: Usually paid out on sales employees based on some targets

- Profits In lieu of Salary: These are covered specifically under Section 17(3) but referred to generally here.

5. Any Advance of Salary

An advance of salary by an employer is taxable in the year it is received by the employee and not in the year to which it pertains. Which is what prohibits the deferral of tax liability.

6. Leave Encashment

Leave salary: Leave salary, or the pay received on encashment of unavailed earned leave, is part of salary as per section 17(1). But leave encashment on retirement or resignation may be exempt under Section 10(10AA) up to limited amount.

7. Annual Accretion to an Unrecognized Provident Fund or a Recognized Provident Fund

The employer’s contribution to an unrecognized provident fund is treated as salary in excess of limits.

8. Transferred Balance in Case of Unrecognized Provident Fund

As per the provisions of section 17(1), the balance transferred from a non-recognised provident fund to a recognised one could be offered to tax as part of salary.

9. Contribution Made by the Central Government or Any Other Employer to New Pension Scheme (NPS) Under Section 80CCD(2)

The employer contribution to NPS is included in the definition of salary for the purposes of this section

Read Also:- Software Engineer Salary | Investment Banker Salary | AI Engineer Salary in India

Does Salary as per Section 17(1) Include HRA?

Yes! Salary as per section 17(1) includes HRA (House Rent Allowance). HRA comes under the broader meaning of salary that is received by an employee from an employer the reason that allowances are one of the elements of ‘salary’ mentioned in this section.

It is noteworthy that the HRA is part of the taxable salary paid first and exemption thereof has to be claimed under section 10(13A) read with rule 2A subject to:

Actual HRA received

- 50% of basic for metro cities or 40% for non-metro cities

- This is rent paid in actual amount – 10% of Salary

Thus though Salary as per section 17(1) includes HRA, the taxable HRA after exemption may be less than or equal to zero depending upon the rent paid by the employee.

Salary as per Section 17(1), 17(2), and 17(3) – Key Differences

The three parts – combo of salary as per section 17(1) 17(2) and 17(3) gives the complete understanding of employment income as per Income Tax Act.

| Feature | Section 17(1) – Salary | Section 17(2) – Perquisites | Section 17(3) – Profits in Lieu of Salary |

| Nature | Regular payments from employer | Non-monetary or indirect benefits | One-time or irregular receipts |

| Examples | Basic pay, wages, HRA, pension, commission | Rent-free accommodation, car facility, ESOP | Compensation on termination, golden handshake |

| Taxability | Fully taxable (subject to exemptions) | Taxable based on prescribed valuation | Fully taxable |

| Exemptions | Section 10(10), 10(10AA), 10(13A), etc. | Section 10(10CC), Rule 3 valuations | Mostly taxable; limited exemptions |

| Government vs. Private | Both | Both (with some distinctions) | Both |

These three sub-sections together constitute the complete definition of income chargeable to tax under the head “Salaries.”

Read Also:- Data Scientist Salary | BSc Nursing Salary

Is Salary as per Section 17(1) Monthly or Yearly?

A lot of taxpayers queries about Salary as per section 17(1) means monthly or yearly?

The short answer is: it is a yearly amount for tax calculation, even if the salary is paid monthly.

Here’s why:

- Income tax is actually the annual tax levied in every financial year (April 1 – March 31).

- Though, the user gets salary every month, in ITR required to present total salary during the year and not the monthly one.

- Form 16 is your income and total tax deducted at source (TDS) for the year, issued by the employer.

- Form 12BA also gives annual perquisite details as well.

This means that, salary as per section 17(1) is monthly or yearly? They collect it every month but it is evaluated and presented annually. In ITR forms, Schedule Salary requires total salary in relation to complete Financial year including all elements under section 17(1).

And if your employer is deducting TDS under section 192, he calculates your annual salary and divides this tax liability on each of the 12 months. Which makes your monthly withholding based on how much tax you owe for the whole year.

Read Also:- RBI Grade B Salary | 4 LPA In Hand Salary | 7 LPA In Hand Salary

Salary as per Section 17(1) – Practical Example

How to understand the salary as per sectikn 17(1) example with a full illustration.

Example: Mr. Ramesh (Private Sector Employee)

| Component | Monthly (₹) | Annual (₹) |

| Basic Salary | 50,000 | 6,00,000 |

| House Rent Allowance (HRA) | 20,000 | 2,40,000 |

| Special Allowance | 10,000 | 1,20,000 |

| Leave Travel Allowance (LTA) | 5,000 | 60,000 |

| Medical Allowance | 1,250 | 15,000 |

| Employer’s NPS Contribution | 5,000 | 60,000 |

| Gross Salary (Section 17(1)) | 91,250 | 10,95,000 |

Here, the Salary as per Section 17(1) is ₹10,95,000 p.a. Basic pay, HRA, allowances, NPS contribution all these components come under section 17 (1).

Having come to this number, the worker would:

- Section 10(13A): HRA Exemption

- Claim Standard Deduction Of ₹75,000 (In Budget 2024-25)

- You can claim allowable deductions for Chapter VI-A (80C, 80D, etc.)

- Arrive at Net Taxable Income

Important Components Table – Salary as per Section 17(1)

Salient Salary components covered under Salary and are deductible under Salary as per section 17(1) of Income Tax Act (Table above) These major earnings contain basic salary, dearness allowance, house rent allowance, special allowance, pension, gratuity, commission and advance salary. There may be a few components which are fully taxable and others will come under partial or complete exemptions under various sections of the Income Tax Act.

For Employees, it is critical to know Salary as per Section 17(1) because it helps in computing the Total Taxable Salary and therefore also helps them plan their Tax Saving Investments appropriately. It also draws special attention to items which are separately recognized as perquisites, under Section 17(2), for example, ESOPs and rent-free accommodation, and compensation under Section 17(3).

With knowledge regarding the tax treatment of each component, taxpayers can strategically control salary components and optimize exemptions available under different sections. Essentially, Salary as per section 17(1) the basis on which salary is taxed in India.

Finally, the complete table detailing the significant components included under Salary as per section 17(1), along with taxability, exemptions, and related sections of the Income Tax Act, can be found here.

| S.No. | Component | Included in Section 17(1)? | Exemption Available? | Relevant Section |

| 1 | Basic Salary/Wages | ✅ Yes | ❌ No | Section 17(1) |

| 2 | Dearness Allowance | ✅ Yes | ❌ No | Section 17(1) |

| 3 | House Rent Allowance | ✅ Yes | ✅ Yes (partial/full) | Section 10(13A) |

| 4 | Leave Travel Allowance | ✅ Yes | ✅ Yes (twice in 4 years) | Section 10(5) |

| 5 | Medical Allowance | ✅ Yes | ❌ No (post 2018) | – |

| 6 | Special Allowance | ✅ Yes | ❌ No | Section 17(1) |

| 7 | Pension | ✅ Yes | ✅ Partial (for govt.) | Section 10(10A) |

| 8 | Gratuity | ✅ Yes | ✅ Yes (limits apply) | Section 10(10) |

| 9 | Leave Encashment | ✅ Yes | ✅ Yes (on retirement) | Section 10(10AA) |

| 10 | Advance Salary | ✅ Yes | ❌ No | Section 17(1) |

| 11 | Commission on turnover | ✅ Yes | ❌ No | Section 17(1) |

| 12 | Employer’s NPS Contribution | ✅ Yes | ✅ Yes (upto 14% for govt.) | Section 80CCD(2) |

| 13 | Rent-Free Accommodation | ❌ No (Perquisite) | Valuations apply | Section 17(2) |

| 14 | ESOP | ❌ No (Perquisite) | Valuations apply | Section 17(2) |

| 15 | Compensation on termination | ❌ No (Profits in lieu) | Section 10(10B) | Section 17(3) |

Read Also:- 20 LPA In Hand Salary | 15 LPA In Hand Salary | 3 LPA in Hand Salary

Salary as per section 17(1) includes pension – Detailed Explanation

Salary as per section 17(1) includes pension, so the pension received from the former employer is overall considered to be the income in the nature of salary under the provisions of Income Tax Act Issues about pension being taxable or exempt arise many of the time with number of tax payers, particularly post retirement. But, commuted pension might be eligible for partial or full exemption based on whether the employee comes from the government or private sector and if you receive gratuity. Also, family pension is not included in under “Salary as per section 17(1) includes pension” but is taxed separately as “Income from Other Sources.” Here is what you need to know:

Types of Pension and Their Tax Treatment

| Pension Type | Included in 17(1)? | Exemption |

| Pension from former employer (uncommuted) | ✅ Yes | No exemption |

| Commuted pension – Government employee | ✅ Yes | Fully exempt u/s 10(10A)(i) |

| Commuted pension – Non-government (with gratuity) | ✅ Yes | 1/3rd of commuted pension exempt |

| Commuted pension – Non-government (without gratuity) | ✅ Yes | 1/2 of commuted pension exempt |

| Family pension (received by widow/dependents) | ❌ No | Taxed under “Other Sources” |

As salary as per section 17(1) includes pension, pensioners receiving pension from a past employer should file their ITR under the heading “Salaries. They also qualify for ₹75,000 (w.e.f. AY 2025-26) Standard Deduction which is exclusive to employees & pensioners.

Computation of Income from Salaries – Step-by-Step

Under the head “Salaries”, computation of taxable income starts with salary as per section 17(1), which comprises almost all important constituents of salary including basic pay, allowances, bonus, commission and pension. Thereafter, the Employers compute salary as per section 17(1) – and add taxable perquisites as per Section 17(2) and profits in lieu of salary as per Section 17(3) to arrive at gross salary.

This is after deducting the exempted allowances under Section 10, such as HRA and LTA. Standard deductions, professional tax, and entertainment allowance are also permissible. Familiarity with salary as per section 17(1) is very important to knowing how much tax will be levied and how to plan their salary properly.

This is illustrated through stepwise computation of taxable income under the head ‘Salaries’ according to the Income Tax Act.

| Step | Item | Amount (₹) |

| Step 1 | Salary as per Section 17(1) | XXX |

| Step 2 | Add: Perquisites u/s 17(2) | XXX |

| Step 3 | Add: Profits in lieu of salary u/s 17(3) | XXX |

| Step 4 | Gross Salary (Total of Steps 1+2+3) | XXX |

| Step 5 | Less: Exemptions under Section 10 (HRA, LTA, etc.) | (XXX) |

| Step 6 | Less: Standard Deduction u/s 16(ia) [₹75,000] | (75,000) |

| Step 7 | Less: Entertainment Allowance u/s 16(ii) [Govt. employees] | (XXX) |

| Step 8 | Less: Professional Tax u/s 16(iii) | (XXX) |

| Step 9 | Net Taxable Income from Salaries | XXX |

The first number in this whole chain of computation as salary as per section 17(1) of income tax act. All deductions and exemptions that follow are applied only to this figure.

Key Distinctions – What is NOT Included in Salary as per Section 17(1)

Although the definition is wide, equally important is what is not considered salary according to the section 17(1):

- Reimbursements: Actual payments made by employer to reimburse employee for expenses incurred on behalf of employer are generally not salary.

- Ex-gratia payment: Discretionary payments without any contract may sometimes fall within the ambit of section 17(3).

- Perquisites: All non-cash perks such as rent-free accommodation, car perqs and ESOPs are taxable under Section 17(2) and not 17(1).

- Payment in lieu of salary / Compensation on termination: As explained under Section 17(3) as profit in lieu of salary.

- Family pension: As mentioned, it is taxable under “Income from Other Sources.”

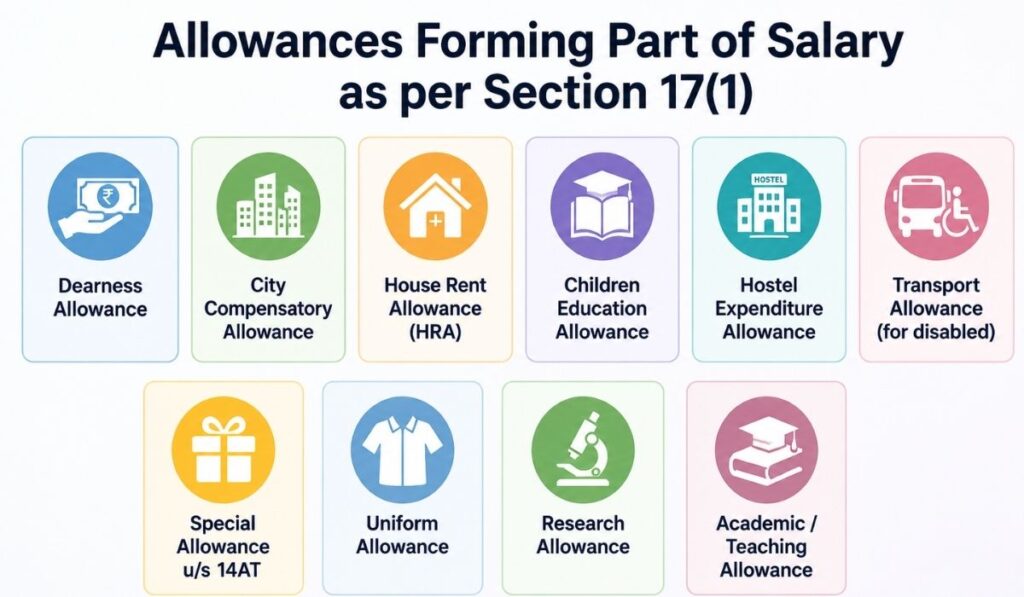

Allowances Forming Part of Salary as per Section 17(1)

salary as per section 17(1), the following allowances are usually a part of salary and are liable to be taxed as income under the Income Tax Act unless provided otherwise. Some of the common taxable allowances are dearness allowance, city compensatory allowance, special allowance,Research allowance, academic allowance. Some allowances such as House Rent Allowance (HRA), children education allowance, hostel expenditure allowance and transport allowance enjoyed by physically challenged assessees may qualify for partial exemption under specific provisions of the Act. Exemptions are, in many cases, only permitted at the level of the real professional cost incurred. By knowing how these allowances come unders alary as per section 17(1)), employees can calculate the taxable salary correctly and can claim the eligible tax benefits in a much more efficient way.

The following allowances table are broadly included in salary as per section 17(1) and are taxable unless a specific exemption is provided:

| Allowance | Taxability | Exemption |

| Dearness Allowance | Fully Taxable | None |

| City Compensatory Allowance | Fully Taxable | None |

| House Rent Allowance | Taxable | Exempt u/s 10(13A) (partial/full) |

| Children Education Allowance | Taxable | ₹100 per child per month (max 2 children) |

| Hostel Expenditure Allowance | Taxable | ₹300 per child per month (max 2 children) |

| Transport Allowance (for disabled) | Taxable | ₹3,200 per month exempt |

| Special Allowance u/s 14A | Taxable | To the extent actually spent for duties |

| Uniform Allowance | Taxable | To the extent spent on uniforms |

| Research Allowance | Taxable | To the extent spent on research |

| Academic/Teaching Allowance | Taxable | To the extent spent |

Relationship Between Section 17(1) and Standard Deduction

The employer will calculate the salary as per section 17(1) (that is a component of Gross Salary) and the employee will deduct the Standard Deduction under base Section 16(ia). Which is a flat type of a deduction without having any proof of the expenditure available here:

- AY 2024-25: ₹50,000

- From AY 2025-26 (Budget 2024): ₹75,000 in New Tax Regime; ₹50,000 in Old Tax Regime

This Standard Deduction can be claimed by employees as well as pensioners and this is where the salary as per section 17(1) includes pension in its ambit.

Salary as per Section 17(1) – Government vs. Private Sector Employees

| Parameter | Government Employees | Private Sector Employees |

| Includes pension? | ✅ Yes | ✅ Yes (if from former employer) |

| Entertainment Allowance deduction? | ✅ Yes (Section 16(ii)) | ❌ No |

| HRA exemption? | ✅ Yes | ✅ Yes |

| Commuted pension exemption? | Fully exempt | Partially exempt (1/3 or 1/2) |

| Gratuity exemption limit? | No limit (fully exempt) | ₹20 lakh (as per latest notification) |

Read Also:- 4.5 LPA In Hand Salary | 12 LPA In Hand Salary | 6 LPA In Hand Salary

Common Mistakes in Reporting Salary as per Section 17(1)

Many a taxpayer or even an HR does mistakes while computing or reporting salary as per Section 17(1). There are the most common:

- Excluding advance salary: Any advance received in the year is chargeable to tax in that year itself not in the relevant assessment year.

- Good Tax Planning: Salary as per section 17(1) includes pension; therefore, the pensioner has to show it under the head “Salaries”

- Mistaking HRA receipt for exemption: HRA should be included at first under Section 17(1), and only then one can claim exemption under Section 10(13A).

- Not treating employer contribution: Towards NPS (not to be included in total salary as per section 17(1) for the purpose of calculating employer contribution under Section 80CCD)

- Salary for reimbursements: Only genuine reimbursements (Actual bill based) are not salary, need to be supported by way of actual claim documents.

Salary as per Section 17(1) – Important Legal Provisions

| Provision | Description |

| Section 17(1) | Definition of “Salary” |

| Section 17(2) | Definition of “Perquisites” |

| Section 17(3) | Definition of “Profits in lieu of Salary” |

| Section 15 | Chargeability of Salary income |

| Section 16 | Deductions from Salary (Standard Deduction, Entertainment Allowance, Professional Tax) |

| Section 10(10) | Exemption on Gratuity |

| Section 10(10A) | Exemption on Commuted Pension |

| Section 10(10AA) | Exemption on Leave Encashment |

| Section 10(13A) | Exemption on HRA |

| Section 10(5) | Exemption on LTA |

| Section 192 | TDS on Salary |

| Rule 2A | Computation of HRA exemption |

Frequently Asked Questions (FAQs)

Q1. What is meant by salary as per section 17(1) of income tax act?

The term salary as per section 17(1) covers the value of every form of remuneration which is received by an employee from the employer by virtue of the employment. It encompasses all aspects of remuneration including basic pay, annuity, pension, gratuity, fees, commission, advance salary and leave encashment, and any other payment as a result of employment.

Q2. Is salary as per section 17(1) monthly or yearly?

While a salary is drawn monthly, it is calculated annually – that is, for income tax purposes, the total income over a financial year (from April 1 to March 31). Both Form 16 & ITR require the annual amount.

Q3. Does salary as per section 17(1) include HRA?

Yes. The Salary as per section 17(1) includes HRA (House Rent Allowance). HRA is an allowance paid by the employer, and from salary definition. Nevertheless, you can claim partial or full exemption under Section 10(13A) depending on the rent you are actually paying, subject to specified limits.

Q4. Does salary as per section 17(1) include pension?

Yes. Salary as per section 17(1) includes pension obtained for the past employment. Pension at a time (monthly) is 100% taxable. Pension commuted (lump sum) is also full exempt subject to tax and the extent of such exemption would depend upon whether the subject is a government or a non governmental employee.

Q5. What is the difference between Section 17(1), 17(2), and 17(3)?

Salary as per section 17(1) 17(2) and 17(3) combined define the income from employment:

17(1) = Salary (indefinite cash payments)

17(2) = Perquisites (tax on non-cash benefits including room, vehicle, ESOPs)

17(3) =Profits in lieu of salary (particular type of payment termed as one time payment in nature)

Q6. Is leave encashment part of salary as per section 17(1)?

Yes. Leave encashment during the course of service is charged under the head of salary. — Section 17(1). Payment in lieu of leave at the time of retirement may be exempt (subject to limits) under Section 10(10AA).

Q7. Are reimbursements included in salary as per section 17(1)?

Generally no. Salary never includes true reimbursements where the employer is reimbursing an employee for actual out of pocket expenditures of the employee made on behalf of the employer. On the other side, flat allowance (for example, a medical allowance paid on a monthly basis without production of bills) is included in the salary under section 17 (1).

Q8. What is the standard deduction available from salary as per section 17(1)?

Under New Tax Regime (AY 2025-26 onwards): The gross salary calculated starting from salary as per section 17(1), a Standard Deduction of ₹75,000 per annum is permitted; Standard Deduction = ₹50,000 (Old Tax Regime)

Q9. Is advance salary taxable under Section 17(1)?

Yes. The advance salary, which is received in the financial year, can be taxable in the same year irrespective of the period in which it relates. Because, in the case of salary, income tax in India is payable on “due or receipt” whichever is earlier.

Q10. Can a pensioner claim standard deduction under Section 16?

Yes. Since salary as per section 17(1) includes pension, pensioners are treated as employees for tax purposes. They are entitled to claim the Standard Deduction of ₹75,000 (New Regime) or ₹50,000 (Old Regime) from their pension income.

Q11. Is commission included in salary as per section 17(1)?

Yes. However, as prescribed in section 17(1), Commission earned by an employee from the employer – on a fixed basis, on turnover or achievement of targets – would fall under the salary ambit and thus will be completely taxable.

Q12. How is HRA exemption calculated when salary as per section 17(1) includes HRA?

HRA exemption under Section 10(13A):For a taxpayer, it is the lowest of the following threeamounts:

Actual HRA received

50% of basic + DA (as defined by divisional MD) Metro areas or 40% of basic + DA (as defined by divisional MD) Non-metro areas

Rent actually paid – 10% of income

HRA included in salary as per section 17(1) is exempt upto this amount.

Conclusion

One of the most basic concept in the Indian income-tax law Salary as per section 17(1). Contrary to common belief salary as per section 17(1) of income tax act is not only limited to basic monthly salary but also includes many forms of employment income viz wages, pension, gratuity, HRA, LTA, Advance salary, Leave encashment, Commission, Employer contribution towards NPS etc.

salary as per section 17(1) means also bring clarity to what should be treated as salaryIn its very definition of salary, all regular inflow is prima facie treated as salary before exemptions, deductions or tax calculation. Whether it is a graduate working out his first salary, a retiree reading how much his pension will be taxed or an HR manager calculating TDS, one needs to have a strong command over this provision.

As a reminder: salary as per section 17(1) is monthly or yearly, in the sense of received monthly but is taxable at the end of the year. Even salary as per section 17(1) includes HRA and salary as per section 17(1) includes pension and it is the most wider basis for salary tax in India.

If you need help with real ITR filing process or, Interpretation of Form 16 or, have these questions, then, get in touch with a chartered accountant who can apply these provisions for you.

🔥 Popular Salary Searches

Dalvi Goyal is a dedicated content writer at TheSalaryInfo.com, specializing in salary insights, career trends, job market updates, and workplace topics. With a strong focus on research and accuracy, Dalvi creates easy-to-understand content that helps students, job seekers, and working professionals make smarter career and financial decisions.